Material Usage Variance

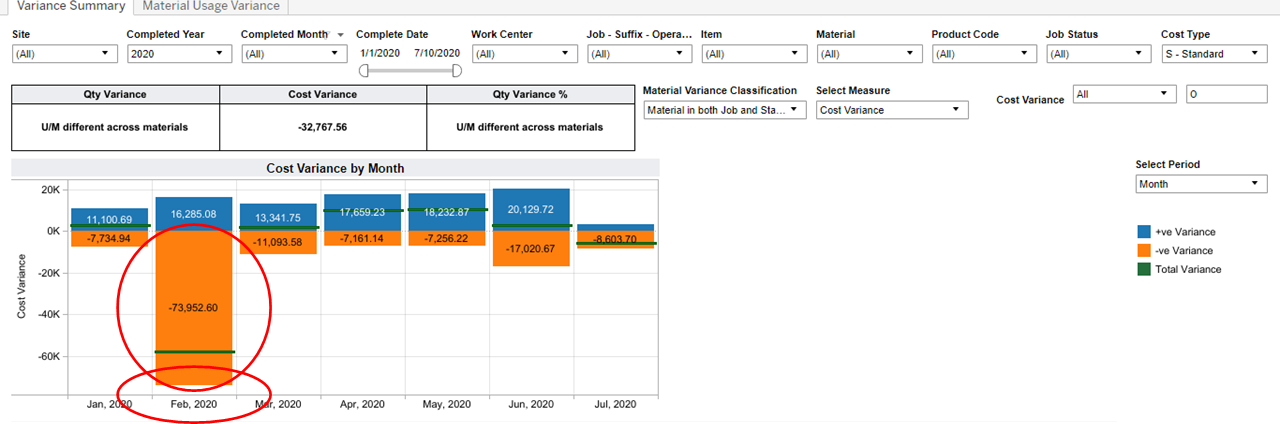

First we will look at Material Usage Variance. Below in Figure 1 we can see a graphical depiction of Material Usage Cost Variance by month for a given period in 2020. It is clear from the dashboard below that there is major discrepancy in the month of February of over $73,000 (see two red ellipses below). If we click on this part of the graph the system will allow us to drill into the detail of the data for that month.

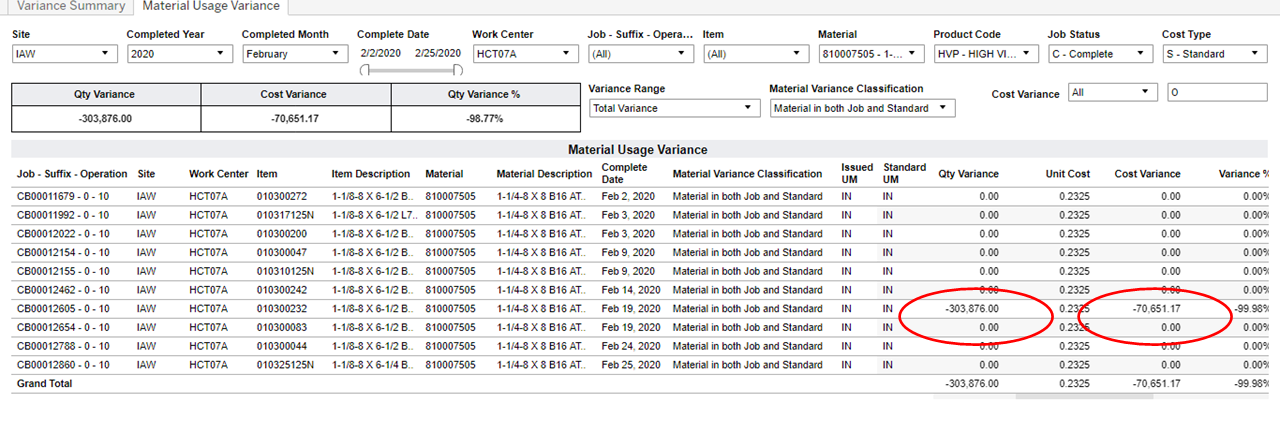

Below we can now see the detail of the data via the Material Usage Variance report below in Figure 2. In the detail below we can see that on February 19th there was a specific Job CB00012605 Operation 10 on Work center HCT07A that had a significant variance in Material usage from what the standard indicates. (see red ellipses below in Figure 2). With this information the management can investigate the Job, and Work Center on this date to understand the nature of the discrepancy.

Production Yield

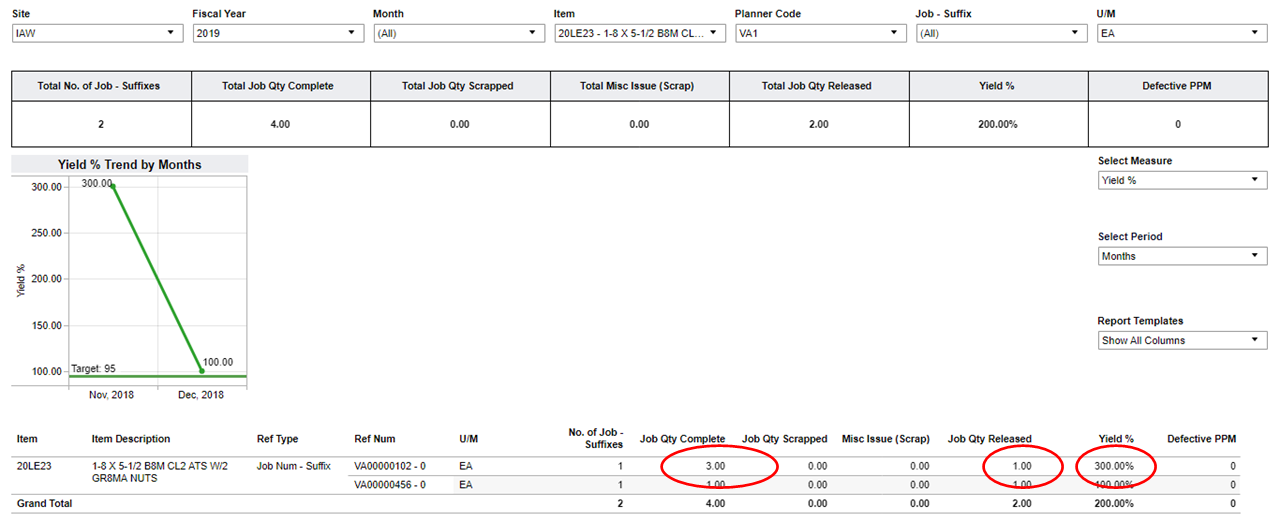

Another important metric is Yield. Yield is often expressed as a percentage. Below in Figure 3 we are looking at a report that shows for Item 20LE23 we are seeing a 300% Yield. This data should immediately be suspect as any Yield exceeding 100% is highly unlikely. If we examine the detail below we can see that the Job had only 1 Item Released, but that 3 Items were reported as being completed. Most likely this is a data entry error. The report below provides the detail the organization would need to correct this error and prevent it from happening in the future.

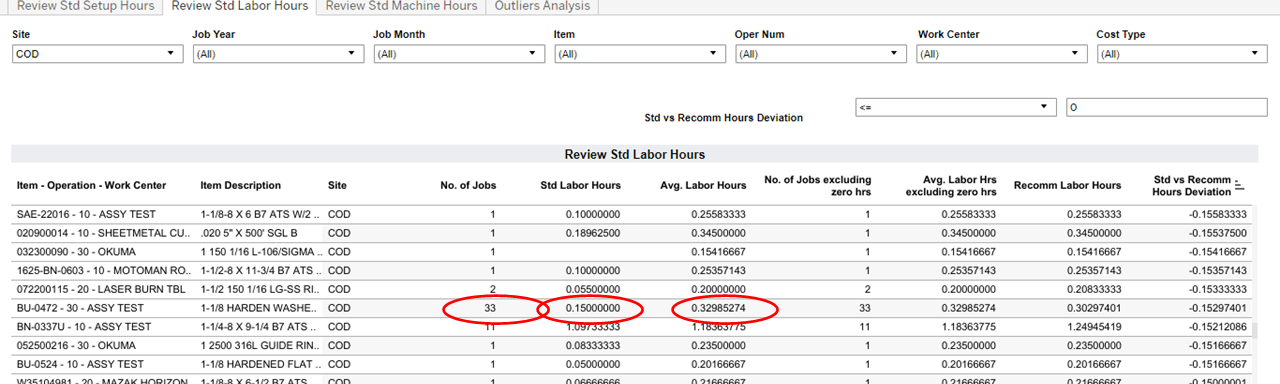

Review Labor Hours

Most manufacturing organizations manage and pay close attention to Labor Hours that go into producing their product. Below in Figure 4 we are looking at a report that shows Labor Hours by Item and Operation. In this data we a particular Item BU-0472 and Operation 30 Assy Test that had a large number of Jobs run (33 in this example) and the Labor Hours are almost double what you would expect from the standard (0.3298 per Item versus the standard of 0.15 per Item) (see three red ellipses below in Figure 4)

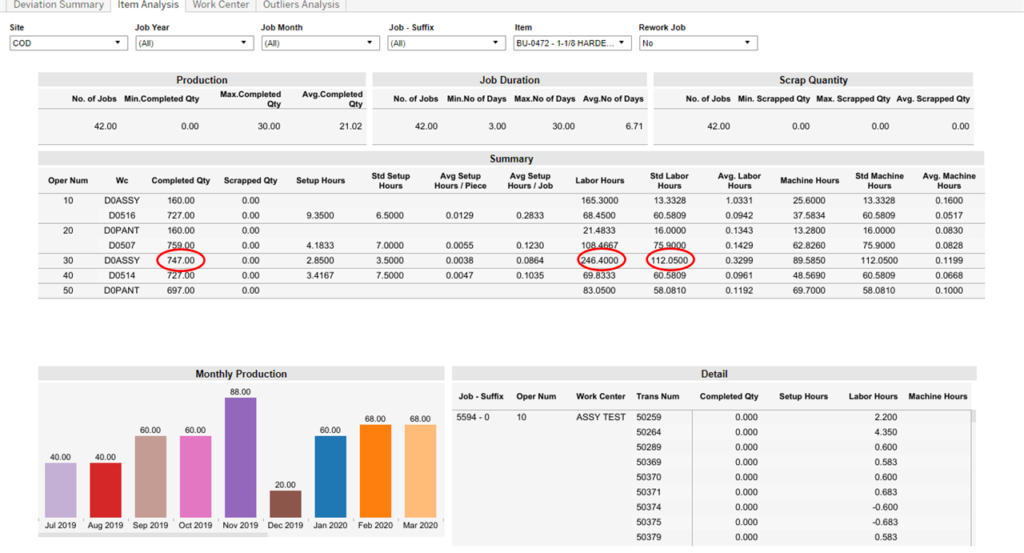

By then moving to the Item Analysis dashboard we can look at specific details of this Item. Below in Figure 5 we can see the total Production activity for this Item over the prior year. We can see that 747 of these items were completed in this time frame. The Standard indicates that this should have taken 112 Labor Hours but in actual fact took 246 Labor Hours (See three red ellipses below in Figure 5)

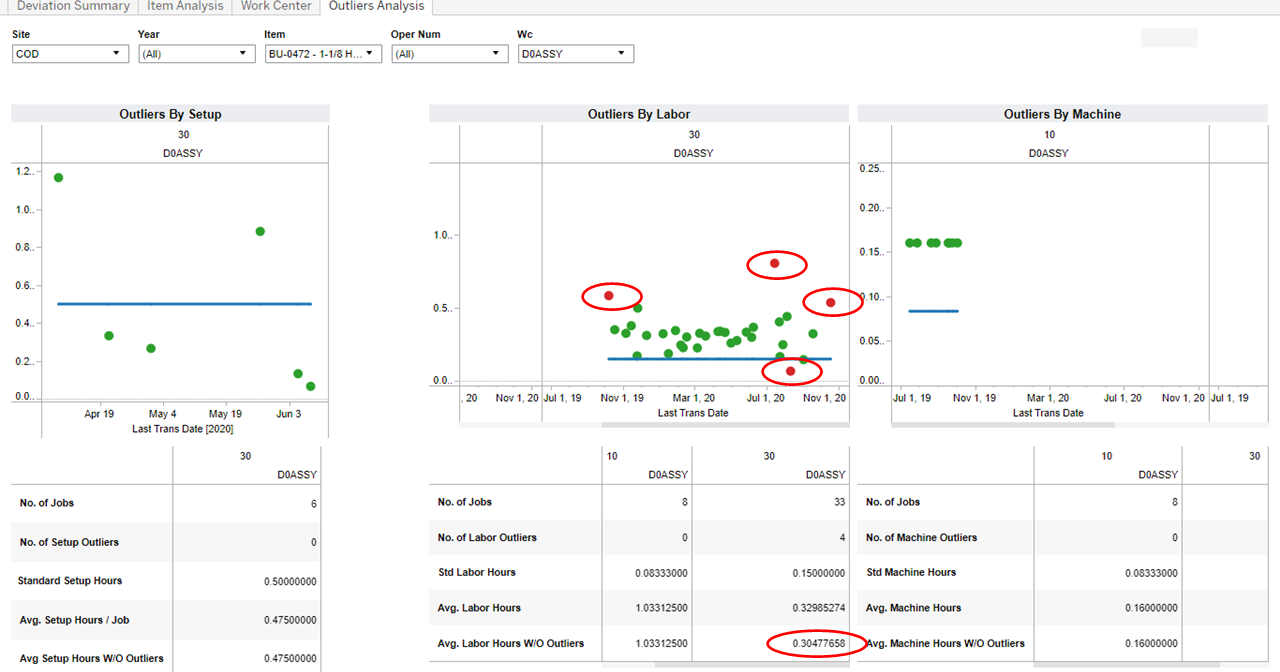

By then looking at the Outlier Analysis we can see which specific Jobs on which Dates may have contributed to the differences in the Actual Hours reported from the Standard Hours. Below in Figure 6 you can see the detail of the different Jobs being plotted by Setup, Labor and Machine Hours. The middle graph shows Labor Hours which we are examining. In it, for Operation 30, the red dots indicate jobs with a significant Variance from the Standard. (see four small red ellipses below). The blue line represents the actual Standard hours for that operation. In this instance we can see the overall number of Jobs, represented by the green dots, still seems to vary significantly from the Standard. If we look below at the Labor Hours expended on these Jobs even with the Outliers removed, the hours at 0.3047 differ significantly from the Standard of 0.15 from this Operation (see large red ellipse below). In this particular case, it is probably an indication that the Standard should be adjusted upward to more realistically reflect the Labor Hours required for this Operation. .